What is Cash Flow ?

What is Cash Flow ?

Cash flow is the net amount of cash and cash equivalents being transferred into and out of a business. Cash received represents inflows, while money spent represents outflows.

At a fundamental level, a company’s ability to create value for shareholders is determined by its ability to generate positive cash flows or, more specifically, maximize long-term free cash flow (FCF). FCF is the cash that a company generates from its normal business operations after subtracting any money spent on capital expenditures (CapEx).

Cash Flow Categories:

1. Cash Flows from Operations (CFO): CFO, or operating cash flow, describes money flows involved directly with the production and sale of goods from ordinary operations. CFO indicates whether or not a company has enough funds coming in to pay its bills or operating expenses. In other words, there must be more operating cash inflows than cash outflows for a company to be financially viable in the long term.

Operating cash flow is calculated by taking cash received from sales and subtracting operating expenses that were paid in cash for the period. Operating cash flow is recorded on a company's cash flow statement, which is reported both on a quarterly and annual basis. Operating cash flow indicates whether a company can generate enough cash flow to maintain and expand operations, but it can also indicate when a company may need external financing for capital expansion.

Note that CFO is useful in segregating sales from cash received. If, for example, a company generated a large sale from a client it would boost revenue and earnings. However, the additional revenue doesn't necessarily improve cash flow if there is difficulty collecting the payment from the customer.

2. Cash Flows from Investing (CFI): CFI, or investing cash flow, reports how much cash has been generated or spent from various investment-related activities in a specific period. Investing activities include purchases of speculative assets, investments in securities, or the sale of securities or assets.

Negative cash flow from investing activities might be due to significant amounts of cash being invested in the long-term health of the company, such as research and development (R&D), and is not always a warning sign.

3. Cash Flows from Financing (CFF): CFF, or financing cash flow, shows the net flows of cash that are used to fund the company and its capital. Financing activities include transactions involving issuing debt, equity, and paying dividends. Cash flow from financing activities provides investors with insight into a company’s financial strength and how well a company's capital structure is managed.

Statement of Cash Flows:

There are three critical parts of a company's financial statements: the balance sheet, the income statement, and the cash flow statement. The balance sheet gives a one-time snapshot of a company's assets and liabilities. The income statement indicates the business's profitability during a certain period.

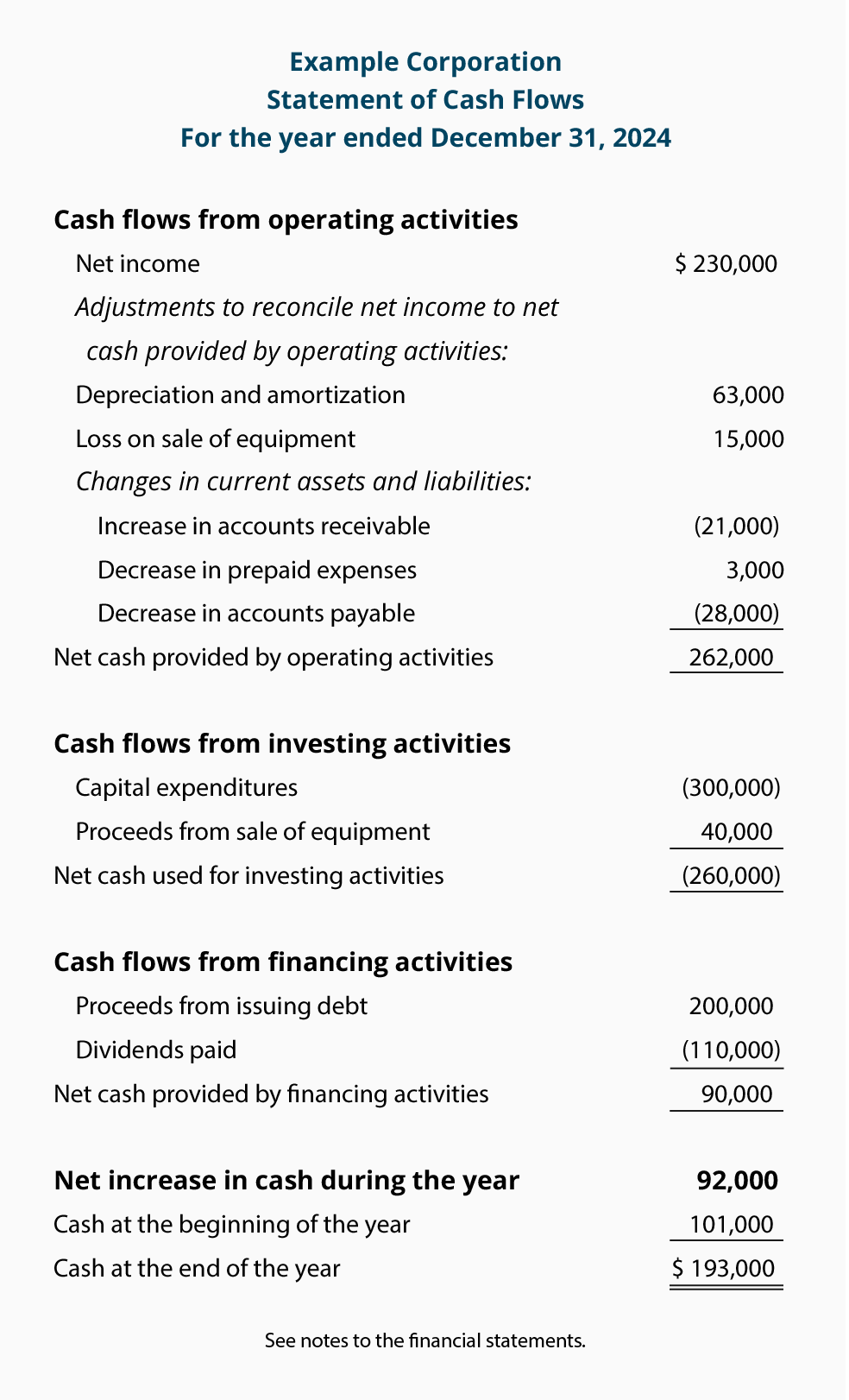

(Image source from: https://www.accountingcoach.com/wp-content/uploads/2013/10/cash-flow-statement-example@2x.png)

The cash flow statement differs from the other financial statements because it acts as a corporate checkbook that reconciles the other two statements. The cash flow statement records the company's cash transactions (the inflows and outflows) during the given period. It shows whether all of the revenues booked on the income statement have been collected.

Analyzing Cash Flows: Using the cash flow statement in conjunction with other financial statements can help analysts and investors arrive at various metrics and ratios used to make informed decisions and recommendations.

- Debt Service Coverage Ratio (DSCR):

Comments

Post a Comment